Table of Contents

The Magic of Consistency: Mastering the Art of the Systematic Investment Plan (SIP)

In the world of finance, there is a recurring myth that you need a massive windfall—a “mountain of gold”—to start building serious wealth. We often picture the stock market as a playground exclusively for the elite, filled with complex tickers and high-stakes gambles.

But what if the most powerful tool for wealth creation wasn’t a secret tip or a lucky break, but a simple, disciplined habit? Enter the Systematic Investment Plan (SIP). It is the financial equivalent of a marathon; it’s not about how fast you run the first mile, but the fact that you keep moving, step by step, until you reach the finish line.

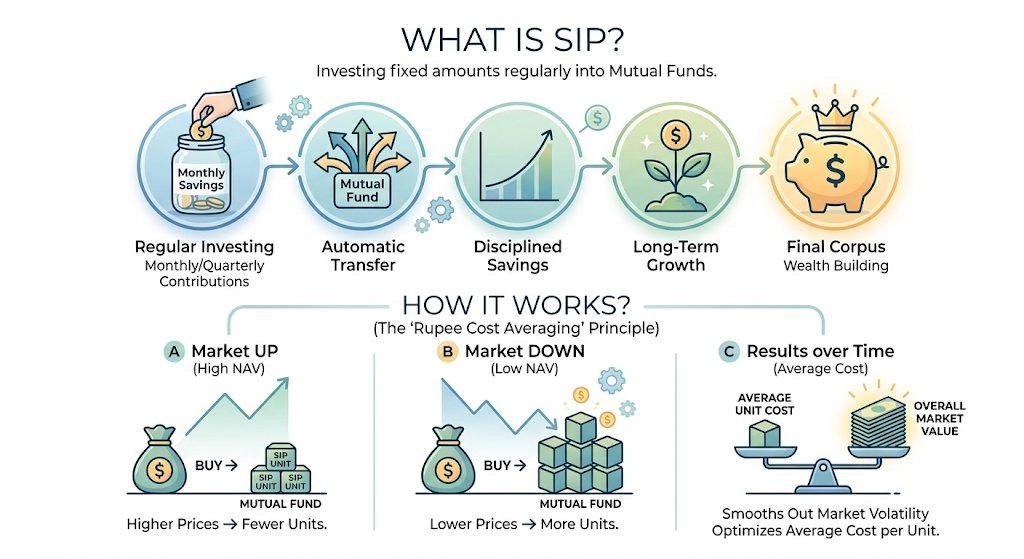

What Exactly is an SIP?

At its core, a Systematic Investment Plan (SIP) is a method of investing a fixed sum of money into a mutual fund at regular intervals—usually monthly, quarterly, or even weekly. Instead of trying to “time the market” by waiting for prices to drop, you invest consistently regardless of market conditions.

Think of it like a subscription service for your future self. Just as you pay for Netflix or Spotify every month, an SIP automates your savings, moving money from your bank account into a chosen investment portfolio.

The Core Philosophy

The SIP philosophy is built on three pillars:

- Discipline: It forces you to save before you spend.

- Averaging: It turns market volatility into an advantage.

- Compounding: It harnesses the “eighth wonder of the world” by staying invested for the long haul.

How Does an SIP Actually Work?

To understand how an SIP functions, we need to look at the mechanics of Net Asset Value (NAV) and Rupee Cost Averaging.

1. The Allocation of Units

When you invest in a mutual fund, you are buying “units.” The price of one unit is called the NAV.

- If the market is up, the NAV is high, and your fixed investment buys fewer units.

- If the market is down, the NAV is low, and your fixed investment buys more units.

2. Rupee Cost Averaging

This is the “secret sauce” of SIPs. Because you are buying more units when prices are low and fewer when prices are high, your average cost per unit over time tends to be lower than the average market price. You essentially stop worrying about whether the market is at a “peak” or a “trough” because the system self-corrects.

3. The Power of Compounding

Compounding happens when the returns on your investment start earning their own returns. In an SIP, the longer you stay invested, the more dramatic the growth becomes.

The mathematical formula for the future value of an SIP is:

$$FV = P \times \frac{(1 + r)^n – 1}{r} \times (1 + r)$$

Where:

- $FV$ = Future Value

- $P$ = Monthly investment amount

- $r$ = Monthly rate of interest (Annual rate / 12)

- $n$ = Number of installments (Months)

Even a small monthly contribution can balloon into a significant corpus over 15 to 20 years because of this exponential growth curve.

Why Choose SIP over Lumpsum?

While a lumpsum investment (investing a large amount all at once) can be profitable if timed perfectly, it carries significant emotional and financial risk. Here is how they compare:

| Feature | SIP | Lumpsum |

| Market Timing | Not required; eliminates guesswork. | Crucial; buying at a peak can hurt returns. |

| Affordability | Start small (often as low as $500). | Requires a large initial capital. |

| Risk Profile | Mitigates volatility through averaging. | Higher risk of immediate capital loss. |

| Psychology | Promotes disciplined, stress-free saving. | Can lead to “investor’s remorse” during dips. |

The Step-by-Step Guide to Starting Your SIP

Starting an SIP is simpler than it has ever been. With modern fintech apps and digital banking, you can set one up in under ten minutes.

Step 1: Define Your Financial Goals

Are you saving for a down payment on a house? Your child’s education? Or a comfortable retirement? Assigning a goal to your SIP helps you stay motivated when the market gets bumpy.

Step 2: Choose the Right Fund Type

Not all SIPs are created equal. You must match the fund to your risk appetite:

- Equity Funds: High risk, high reward. Best for long-term goals (7+ years).

- Debt Funds: Lower risk, steady returns. Good for short-to-medium-term goals.

- Hybrid Funds: A mix of both, providing a balanced approach.

Step 3: Determine the Amount and Frequency

Be realistic. It is better to start a small SIP that you can maintain for ten years than a large one that you have to cancel after six months because of a cash crunch.

Step 4: Automate the Process

Set up an “Auto-debit” or “Bank Mandate.” By automating the transfer, you remove the “choice” of whether to invest or spend, ensuring your financial goals stay on track.

Common Myths vs. Reality

Despite their popularity, several misconceptions surround SIPs. Let’s clear the air:

Myth: SIPs are only for small investors.

Reality: While SIPs are accessible for small investors, many high-net-worth individuals use them to manage liquidity and reduce the risk of entering a volatile market with millions at once.

Myth: You cannot stop an SIP once started.

Reality: SIPs offer incredible flexibility. You can pause, stop, or increase (Top-up) your investment at any time without heavy penalties.

Myth: SIPs guarantee positive returns.

Reality: SIPs are a method of investing, not a guarantee. They are subject to market risks. However, historically, the probability of negative returns decreases significantly as the investment duration increases beyond 5–7 years.

Strategies for Success: “The Pro Moves”

If you want to take your SIP journey from “good” to “extraordinary,” consider these advanced strategies:

1. The Step-Up SIP

Increase your SIP amount annually in line with your salary hikes. Even a 10% annual increase in your SIP contribution can nearly double your final corpus over long periods.

2. Don’t Fear the Dip

When the market crashes, the natural instinct is to panic and stop the SIP. This is a mistake. A market dip is when your SIP works hardest, buying more units at “sale” prices. Continuing your SIP during a bear market is the single most effective way to build wealth.

3. Review, Don’t React

Check your portfolio once or twice a year to ensure the fund is performing well compared to its benchmark. Do not check it daily; the “noise” of daily market fluctuations will only lead to emotional decision-making.

The Psychological Edge: Peace of Mind

Beyond the numbers, the greatest benefit of an SIP is psychological freedom.

We live in an era of information overload. Every day, news headlines scream about inflation, geopolitical tensions, or interest rate hikes. Trying to navigate these as an individual investor is exhausting. An SIP acts as a shield. It allows you to ignore the noise, knowing that your wealth is growing quietly in the background while you focus on your career, your family, and your life.

Conclusion: The Best Time to Start was Yesterday

In finance, there is a famous saying: “The best time to plant a tree was 20 years ago. The second best time is now.”

The math of an SIP is undeniable—time is a much more powerful factor than the amount invested. By starting today, even with a modest sum, you are giving your money the time it needs to grow, compound, and eventually provide you with the financial freedom you deserve.

The journey to financial independence doesn’t require a miracle. It just requires a system. Start your SIP today, stay the course, and let time do the heavy lifting.

Disclaimer

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or professional advice. Investing in Mutual Funds through a Systematic Investment Plan (SIP) involves market risks, including the possible loss of principal. Past performance is not a reliable indicator of future results. Before making any investment decisions, it is recommended that you:

- Conduct your own research or consult with a certified financial advisor.

- Assess your risk appetite and financial goals thoroughly.

- Read all scheme-related documents carefully to understand the specific risks associated with any fund.

The author and publisher are not responsible for any financial losses or decisions made based on the content of this article.