FACTSHEET IS THE WAY TO KNOW EVERYTHING ABOUT MUTUAL FUND.

What is a Mutual Fund Factsheet — And Why Every Investor Should Read It

A factsheet is the monthly report card of a mutual fund. It tells you everything from where your money is invested to how the fund manager has performed over time — if you know how to read it.

Every mutual fund in India is legally required to publish a factsheet every month. Yet most retail investors never open one. Understanding what’s inside can transform how you pick, track, and exit mutual fund investments.

Whether you are a first-time investor just starting your SIP journey or a seasoned market participant managing a large portfolio, the mutual fund factsheet is your single most important reference document. It gives you a transparent, standardised snapshot of the fund — its holdings, its risks, its costs, and its performance — all in one place.

In this guide, we break down every section of a factsheet, explain what the big numbers mean (like a ₹25,000 crore AUM), and reveal how large fund houses actually manage that enormous pile of public money.

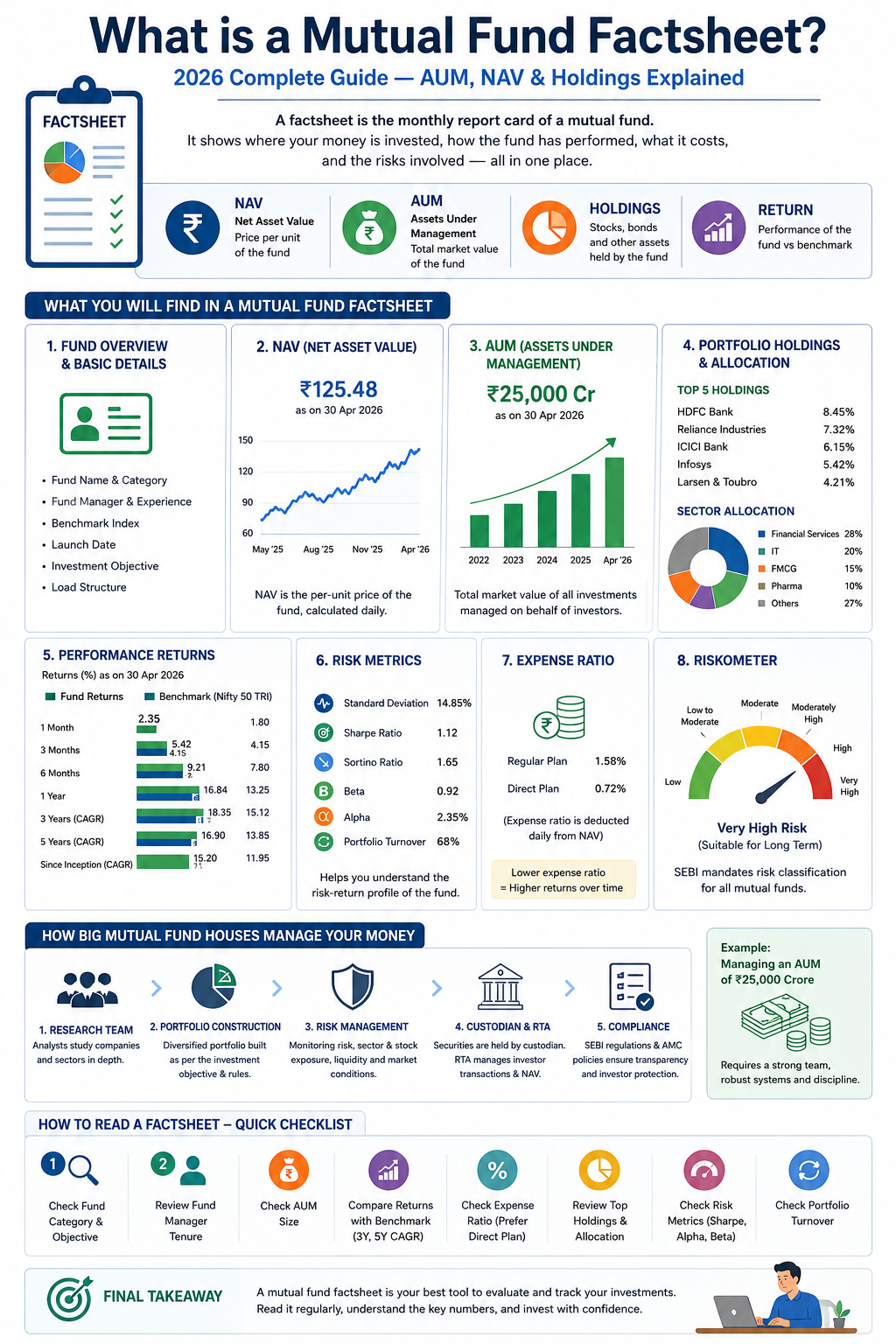

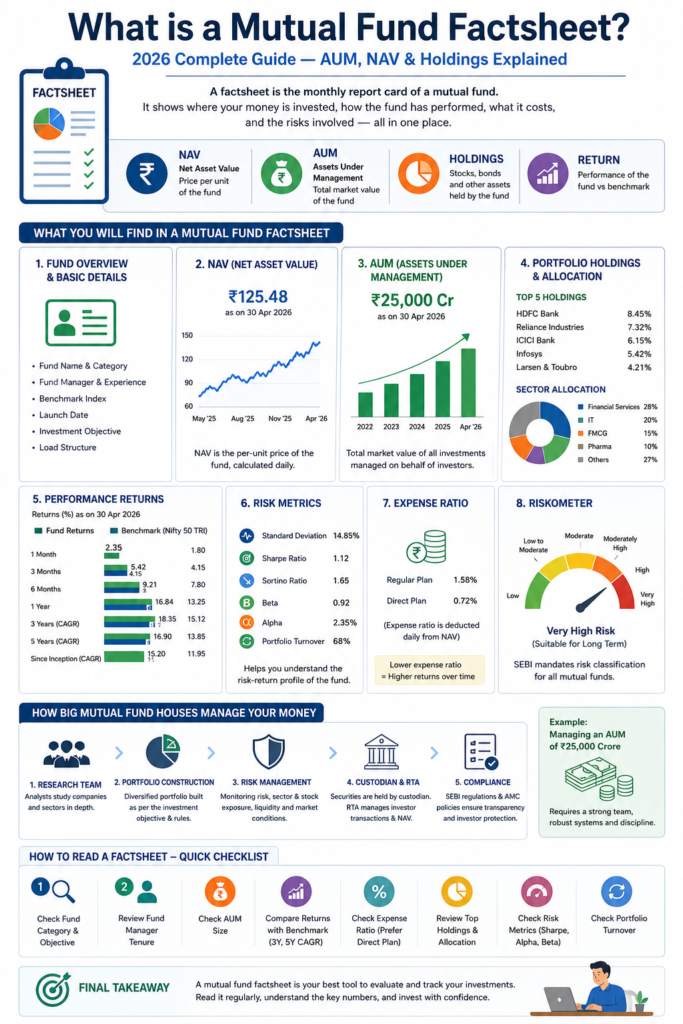

What is a Mutual Fund Factsheet?

A mutual fund factsheet — also called a fund card or monthly factsheet — is an official document published by an Asset Management Company (AMC) every month. It summarises the complete health of a scheme: where it invests, how it has performed, what it costs, and who is managing it.

SEBI (Securities and Exchange Board of India) mandates that all AMCs publish factsheets within 10 days of the end of each month. This means if you want information as of March 31, the updated factsheet should be out by April 10.

A factsheet is essentially a mutual fund’s monthly report card — a standardised, SEBI-regulated document that tells investors exactly what the fund owns, how it has performed, and what it costs to hold. Unlike marketing brochures, factsheets are data-heavy and designed for informed decision-making.

Think of it this way: if you were buying a flat, you’d want to know the location, the builder’s track record, the amenities, the floor plan, and the price per sq. ft. A factsheet does exactly the same job for a mutual fund investment — it gives you all the material facts, not just the headline returns.

What Information Does a Factsheet Provide?

A typical mutual fund factsheet is packed with information across multiple sections. Here is a detailed breakdown of each section and what it means for you as an investor.

1. Fund Overview & Basic Details

The first section of any factsheet gives you the identity card of the fund. It includes:

| Field | What It Means |

|---|---|

| Fund Name & Category | The official name (e.g., Mirae Asset Large Cap Fund) and SEBI category (large cap, flexi cap, mid cap, etc.) |

| Fund Manager | The person managing your money, along with their total experience and years managing this specific fund |

| Benchmark Index | The index the fund targets to beat — e.g., Nifty 50 TRI or BSE Sensex TRI |

| Launch Date (NFO Date) | When the fund was first launched; older funds have longer track records to evaluate |

| Investment Objective | A brief description of the fund’s stated goal — capital appreciation, income generation, or both |

| Load Structure | Exit load (penalty for early exit) and entry load details (mostly nil now) |

2. NAV — Net Asset Value

The NAV is the per-unit price of the fund on a given date. It is calculated daily by dividing the total value of all assets in the fund’s portfolio (minus liabilities) by the total number of units outstanding.

A common misconception is that a fund with a higher NAV (say ₹500) is expensive compared to one at ₹20. This is incorrect — the NAV only reflects the price per unit, not the “cheapness” of the fund. What matters is the percentage growth in NAV over time.

3. Assets Under Management (AUM) — The Big Number

AUM is the total market value of all investments the fund manages on behalf of its investors. When you read “this fund has an AUM of ₹25,000 crore,” it means investors have collectively put ₹25,000 crore into this fund, and the fund manager is investing all of it on their behalf.

AUM size matters for a few reasons. A very large AUM can make it harder for the fund manager to enter and exit positions in small-cap or mid-cap stocks without moving the market. Conversely, a very small AUM (under ₹100 crore) can signal low investor confidence or a very new fund without a track record.

4. Portfolio Holdings & Allocation

This is arguably the most important section of the factsheet. It shows exactly what the fund owns — typically the top 10 holdings by weight, plus the sector-wise and market-cap-wise allocation.

When reviewing holdings, check whether the fund is over-concentrated in a single stock or sector. SEBI rules cap individual stock exposure at 10% of AUM, but you should still watch for heavy clustering in one sector or theme.

5. Performance Returns

Returns are shown across multiple time periods — 1 month, 3 months, 6 months, 1 year, 3 years, 5 years, 10 years, and since inception. Both absolute returns and annualised returns (CAGR) are provided, always alongside the benchmark index returns for comparison.

6. Risk Metrics

Many investors skip this section — and that is a mistake. Risk metrics tell you how bumpy the ride has been to achieve those returns.

| Risk Metric | What It Tells You |

|---|---|

| Standard Deviation | How much the fund’s returns fluctuate around the average. Higher = more volatile. |

| Sharpe Ratio | Return earned per unit of risk. Higher is better. Above 1.0 is considered good. |

| Sortino Ratio | Like Sharpe, but only penalises downside volatility. More useful for equity funds. |

| Beta | How much the fund moves relative to the market. Beta of 0.9 means the fund moves 90% as much as the index. |

| Alpha | Excess return over the benchmark. Positive alpha = fund manager is adding value. |

| Portfolio Turnover | How frequently the fund buys and sells holdings. High turnover = high transaction costs. |

7. Expense Ratio

This is the annual fee charged by the AMC to manage the fund, expressed as a percentage of AUM. It is deducted daily from the fund’s NAV — you never pay it separately, but it silently reduces your returns.

Over a 20-year investment horizon, the difference between a 0.5% and 1.5% expense ratio on a ₹10 lakh investment can be several lakhs of rupees. Always check expense ratio — especially if comparing a Regular plan and Direct plan of the same fund.

8. Riskometer

SEBI mandates that every factsheet display a riskometer — a dial-style illustration showing the risk level of the fund from Low to Very High. This is especially useful for investors comparing funds across categories like liquid funds vs. small cap funds.

How Do Big Mutual Fund Houses Manage Thousands of Crores?

When a fund has ₹25,000 crore in AUM, the management process becomes extremely structured and institutional. Here’s how large AMCs actually deploy, monitor, and protect that enormous pool of capital.

Investment Policy Statement (IPS) — The Rule Book

Every fund operates under a SEBI-approved Scheme Information Document (SID) and a detailed Investment Policy Statement. This lays down which stocks are eligible, what concentration limits apply, which sectors can be overweighted, and what minimum credit ratings are acceptable for debt holdings. No fund manager can deviate from this rule book without approval.

Research Teams & Analyst Coverage

Large AMCs like SBI Mutual Fund, HDFC AMC, or ICICI Prudential employ teams of 20–40+ research analysts. Each analyst covers a specific sector — banking, pharma, IT, auto — and produces detailed reports and earnings models for every stock in their universe. Fund managers make buy/sell decisions based on this research, supported by Bloomberg terminals, broker research, and company meetings.

Portfolio Construction & Diversification

For a ₹25,000 crore large-cap fund, the manager might hold 40–70 stocks across 8–12 sectors. Concentration limits set by SEBI ensure no single stock exceeds 10% of the portfolio. For equity funds, the portfolio is typically rebalanced quarterly or when significant market events occur, while maintaining liquidity through a mix of cash and liquid assets (usually 2–5%).

Risk Management & Compliance

A separate Risk Management team runs independent oversight. They track Value at Risk (VaR), stress-test scenarios, and monitor tracking error (for index funds). Compliance officers ensure every trade adheres to SEBI regulations, and any breach — even a small one — triggers an automatic alert. Trustees appointed under the fund’s trust structure hold the ultimate fiduciary responsibility for investor money.

Managing Inflows & Outflows (Liquidity Management)

This is one of the trickiest parts of managing a large fund. On any given day, thousands of SIPs are being invested while other investors are redeeming units. The fund must always have enough liquidity to honour redemption requests within T+2 business days. Large fund managers maintain a buffer of liquid holdings and carefully time their equity purchases to avoid moving the market price of mid/small cap stocks.

Custodian, Registrar, and Settlement

The actual securities held by the fund are not kept with the AMC — they are held by a SEBI-registered custodian (like Deutsche Bank, HDFC Bank, or Citibank). The Registrar and Transfer Agent (RTA) — either CAMS or KFintech — manages all investor records, processes transactions, and handles NAV calculations. This separation protects investors even if the AMC itself faces financial trouble.

Understanding AUM Size — What Does ₹25,000 Crore Mean?

To put the scale in perspective: ₹25,000 crore is ₹250 billion — larger than the annual budget of several Indian states. Managing this is not a one-person job but an institutional machine with dozens of teams, sophisticated systems, and real-time monitoring.

“A large AUM creates a certain market gravity — the fund itself can move prices when it buys or sells. The best managers are those who can deploy capital efficiently without tipping off the market.”

How to Read a Factsheet — Step-by-Step Checklist

When you download a factsheet (available on the AMC’s website and AMFI website), here’s a practical sequence to follow:

| Step | What to Check |

|---|---|

| Step 1 — Verify Category | Confirm the fund matches your investment goal — large cap for stability, mid/small cap for growth, hybrid for balance. |

| Step 2 — Check Fund Manager Tenure | Ideally, the fund manager should have been managing this specific fund for at least 3–5 years. Recent changes can alter the fund’s style. |

| Step 3 — Review AUM Size | Too small (<₹100 cr) or too large (for small cap) are both red flags. |

| Step 4 — Compare Returns vs Benchmark | Check 3-year and 5-year CAGR against the stated benchmark. Consistent outperformance matters, not just one good year. |

| Step 5 — Check Expense Ratio | For equity funds, prefer direct plans under 1%. High expense ratios are a permanent drag on returns. |

| Step 6 — Review Top Holdings | The top 10 holdings shouldn’t exceed 50–60% of the portfolio. Excessive concentration = higher risk. |

| Step 7 — Check Sharpe Ratio | Compare across peer funds in the same category. A higher Sharpe means better risk-adjusted returns. |

| Step 8 — Review Portfolio Turnover | For equity funds, turnover above 80–100% per year means high churn, which increases transaction costs. |

Frequently Asked Questions

Where can I find a mutual fund factsheet?

All AMC websites publish factsheets in their “Downloads” or “Factsheet” section. You can also access them through AMFI’s website (amfiindia.com). Platforms like Zerodha Coin, Groww, and MF Central also link to factsheets within each fund’s detail page.

Is a factsheet the same as a Scheme Information Document (SID)?

No. The SID is a permanent, detailed legal document that describes the fund’s structure when it was launched. A factsheet is a monthly updated snapshot of the fund’s current portfolio, performance, and metrics. You need both — the SID to understand rules and objectives, the factsheet to track current health.

How often should I read the factsheet of my fund?

For long-term SIP investors, once a quarter is sufficient. Pay closer attention if: the fund manager changes, the AUM grows sharply (especially for small/mid caps), or the fund’s returns significantly lag its benchmark for 2+ consecutive years.

Does a high AUM guarantee good performance?

Not at all. AUM reflects trust and past track record, but large funds can sometimes become “closet indexers” — their portfolio begins to look too similar to the index because they can’t deploy large sums into high-conviction bets. Always check alpha and tracking error alongside AUM.

Can a mutual fund factsheet be misleading?

The data itself is accurate — it’s SEBI-regulated. But point-in-time metrics can be misleading. For example, short-term returns can spike due to luck, and the portfolio disclosed is a month-old snapshot (not real-time). Always look at rolling returns over 3–5 year periods rather than trailing returns from a single date.

Final Takeaway

A mutual fund factsheet is not a marketing document — it is a data-rich transparency tool. It shows you where your money is going, who is managing it, what they are charging, and whether they are earning their fee. In a country where millions of people are investing in mutual funds through SIPs, learning to read a factsheet is one of the most valuable financial skills you can develop.

The big AMCs managing ₹10,000–₹80,000 crore funds are doing so through institutional-grade research teams, robust risk management, custodial structures, and SEBI oversight. Your money is protected by multiple layers of regulation — but it is your responsibility to make sure it is in the right fund, tracked periodically, and aligned with your goals.

Start with one factsheet this month. Pick any fund you already hold, download the latest factsheet from the AMC website, and go through each section using the checklist above. Within 20 minutes, you will know your fund better than 90% of investors who hold it.