Mutual Funds Explained: Expense Ratio, Sharpe Ratio & Key Metrics Every Investor Must Know (2026 Guide)

Table of Contents

What Are Mutual Funds?

A mutual fund is a professionally managed investment vehicle that pools money from multiple investors to purchase a diversified portfolio of stocks, bonds, or other securities. Each investor owns “units” or “shares” of the fund, and the fund’s performance is distributed proportionally.

In India alone, the mutual fund industry managed over ₹65 lakh crore in Assets Under Management (AUM) as of 2025, reflecting the explosive growth in retail participation. In the US, the industry manages over $25 trillion in assets.

Whether you are a first-time investor or a seasoned market participant, understanding the key metrics and ratios of mutual funds is not optional — it is essential for making informed financial decisions.

How Mutual Funds Work

When you invest in a mutual fund:

- Your money is pooled with thousands of other investors.

- A fund manager (or a team) actively or passively manages the portfolio.

- The fund invests in securities aligned with its stated objective (e.g., large-cap equities, government bonds, gold).

- Your returns are a reflection of the underlying portfolio’s performance, minus costs.

The beauty of mutual funds lies in diversification — even a small investment of ₹500 or $50 via a SIP (Systematic Investment Plan) gives you exposure to dozens or hundreds of securities.

Types of Mutual Funds

Before diving into metrics, here is a quick overview of the main categories:

- Equity Mutual Funds — Invest primarily in stocks; higher risk, higher potential returns.

- Debt Mutual Funds — Invest in fixed-income instruments like bonds; relatively lower risk.

- Hybrid Mutual Funds — A mix of equity and debt to balance risk and return.

- Index Funds — Passively track a market index such as Nifty 50 or S&P 500.

- ELSS (Equity Linked Savings Scheme) — Tax-saving funds under Section 80C in India with a 3-year lock-in.

- Liquid Funds — Invest in very short-term instruments; ideal for parking emergency funds.

- International Funds — Invest in foreign markets for global diversification.

- Sectoral/Thematic Funds — Concentrated exposure to specific industries like technology, pharma, or banking.

Each type comes with its own risk profile and ideal investor profile.

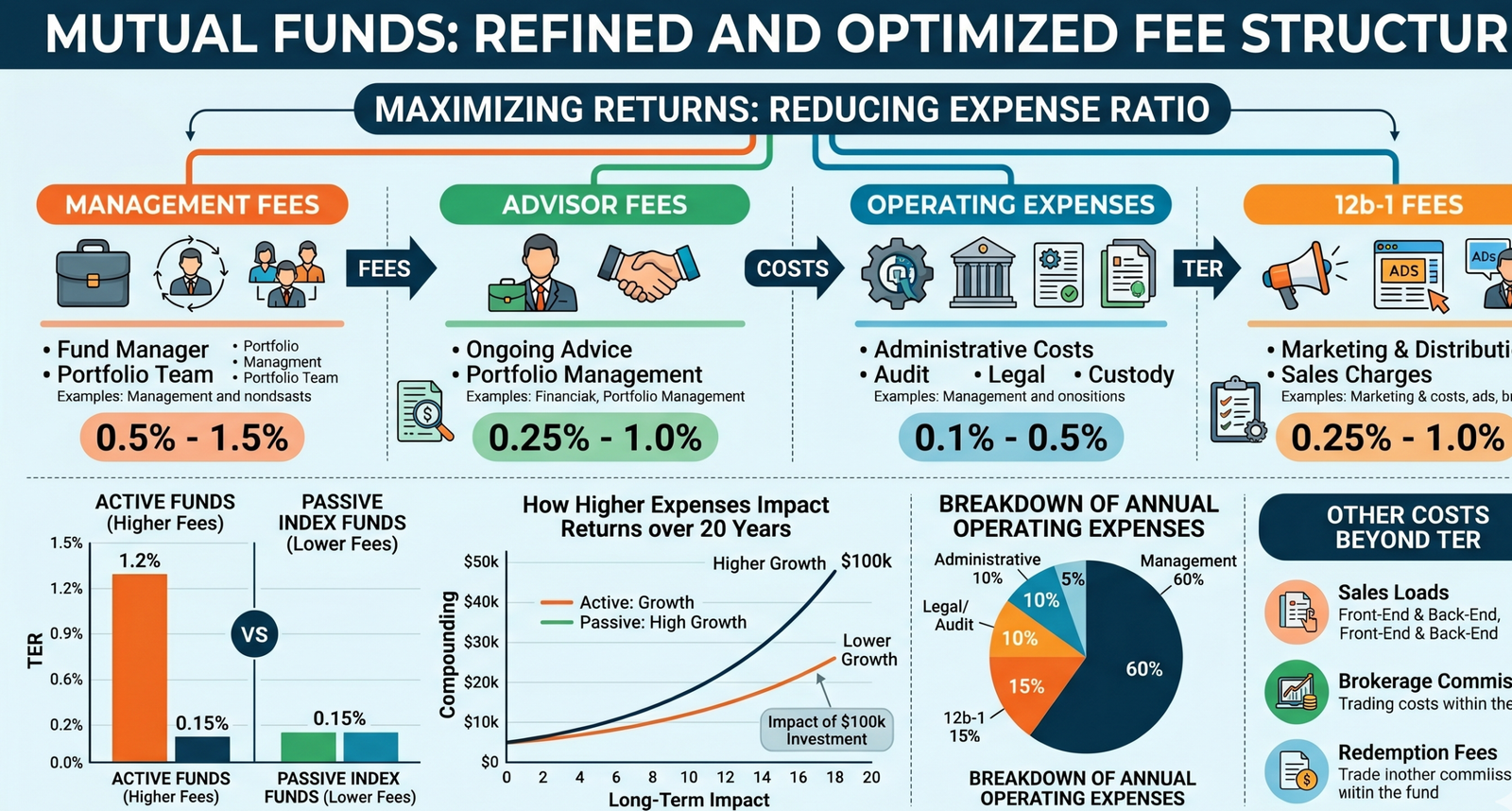

Expense Ratio: The Silent Return Killer

What Is the Expense Ratio?

The expense ratio is the annual fee that a mutual fund charges its investors to cover operating costs, including fund management fees, administrative expenses, marketing costs, and regulatory fees. It is expressed as a percentage of the fund’s total assets.

Formula:

Expense Ratio = (Total Annual Fund Expenses ÷ Average AUM) × 100

Why Does the Expense Ratio Matter?

The expense ratio is deducted from the fund’s NAV on a daily basis — meaning you never see it as a direct charge, but it silently erodes your returns over time.

Example: Suppose two funds both generate a gross return of 12% per year.

- Fund A has an expense ratio of 0.10% (index fund)

- Fund B has an expense ratio of 1.50% (actively managed fund)

Over 20 years on a ₹1 lakh investment:

- Fund A grows to approximately ₹8.62 lakh

- Fund B grows to approximately ₹7.14 lakh

The difference? Over ₹1.48 lakh — lost entirely to fees!

What Is a Good Expense Ratio?

| Fund Type | Low (Good) | Average | High (Expensive) |

|---|---|---|---|

| Index/ETF | 0.05% – 0.20% | 0.20% – 0.50% | Above 0.50% |

| Active Equity | 0.50% – 1.00% | 1.00% – 1.50% | Above 2.00% |

| Debt Funds | 0.20% – 0.50% | 0.50% – 1.00% | Above 1.50% |

Pro Tip: SEBI in India has imposed TER (Total Expense Ratio) limits based on AUM slabs. Always opt for Direct Plans over Regular Plans — they have a 0.5%–1.5% lower expense ratio since there is no distributor commission.

Sharpe Ratio: Measuring Risk-Adjusted Returns

What Is the Sharpe Ratio?

Developed by Nobel laureate William F. Sharpe, the Sharpe ratio measures the return earned per unit of total risk taken. It helps investors understand whether a fund’s returns are the result of smart investing decisions or excessive risk-taking.

Formula:

Sharpe Ratio = (Fund Return − Risk-Free Rate) ÷ Standard Deviation of Fund Returns

- Fund Return: The annualised return of the mutual fund.

- Risk-Free Rate: Typically the return on a government bond or a fixed deposit (e.g., 6.5% in India).

- Standard Deviation: The volatility of the fund’s returns.

How to Interpret the Sharpe Ratio

| Sharpe Ratio | Interpretation |

|---|---|

| Below 1.0 | Poor — risk not adequately compensated |

| 1.0 – 1.99 | Good — decent risk-adjusted performance |

| 2.0 – 2.99 | Very Good — strong performance |

| 3.0 and above | Excellent — outstanding risk-adjusted returns |

Example:

- Fund X returns 14%, risk-free rate is 6.5%, standard deviation is 15%

- Sharpe Ratio = (14 − 6.5) ÷ 15 = 0.50 (Not great)

- Fund Y returns 14%, risk-free rate is 6.5%, standard deviation is 9%

- Sharpe Ratio = (14 − 6.5) ÷ 9 = 0.83 (Better!)

Both funds delivered the same return — but Fund Y did so with significantly less volatility, making it the superior choice from a risk-adjusted perspective.

Alpha: Are Fund Managers Adding Value?

What Is Alpha?

Alpha represents the excess return of a mutual fund compared to its benchmark index after adjusting for risk. A positive alpha means the fund manager has generated returns above what the market would have delivered. A negative alpha means underperformance.

Formula:

Alpha = Fund Return − [Risk-Free Rate + Beta × (Benchmark Return − Risk-Free Rate)]

Interpreting Alpha

- Positive Alpha (+2): The fund outperformed its benchmark by 2% on a risk-adjusted basis — excellent.

- Zero Alpha: The fund matched its benchmark — similar to owning an index fund.

- Negative Alpha (−1.5): The fund underperformed the benchmark by 1.5% — the manager destroyed value.

For actively managed funds, consistent positive alpha over 3–5 years is the primary justification for paying a higher expense ratio. If a fund consistently shows negative or near-zero alpha, switching to a low-cost index fund makes far more economic sense.

Beta: Understanding Market Sensitivity

What Is Beta?

Beta measures a mutual fund’s sensitivity to movements in its benchmark index. It indicates how much the fund’s value is likely to change when the market moves by a certain percentage.

| Beta Value | Meaning |

|---|---|

| Beta = 1.0 | Fund moves in line with the market |

| Beta > 1.0 | Fund is more volatile than the market (aggressive) |

| Beta < 1.0 | Fund is less volatile than the market (defensive) |

| Beta < 0 | Fund moves inversely to the market (rare) |

Example: A fund with a beta of 1.3 means that if the Nifty 50 rises by 10%, the fund is expected to rise by 13%. Conversely, if the index falls by 10%, the fund may fall by 13%.

Who Should Care About Beta?

- Conservative investors and retirees should prefer low-beta funds.

- Aggressive growth investors may prefer high-beta funds during bull markets.

- Beta is especially useful when combined with the Treynor Ratio (explained later).

Standard Deviation: Gauging Volatility

What Is Standard Deviation in Mutual Funds?

Standard deviation measures the degree to which a fund’s returns deviate from its average (mean) return over a specific period. It is the most widely used measure of total risk in a portfolio.

A higher standard deviation means the fund’s returns are more unpredictable — swinging wildly from highs to lows. A lower standard deviation indicates steadier, more consistent returns.

Example:

- Fund A: Average annual return of 12% with a standard deviation of 5% → returns typically range from 7% to 17%

- Fund B: Average annual return of 12% with a standard deviation of 20% → returns typically range from −8% to 32%

Both funds have the same average return, but Fund A offers far more predictable outcomes for conservative investors.

Sortino Ratio: A Smarter Risk Metric

The Sortino Ratio is a refinement of the Sharpe Ratio. The key difference? While the Sharpe Ratio penalises both upside and downside volatility, the Sortino Ratio only penalises downside volatility — which is the risk most investors actually care about.

Formula:

Sortino Ratio = (Fund Return − Risk-Free Rate) ÷ Downside Deviation

A higher Sortino Ratio indicates better risk-adjusted performance, specifically relative to harmful downside risk. For equity funds that experience large temporary drawdowns, the Sortino Ratio is often a more meaningful metric than the Sharpe Ratio.

NAV (Net Asset Value): What It Really Means

What Is NAV?

NAV (Net Asset Value) is the per-unit price of a mutual fund. It is calculated at the end of every trading day.

Formula:

NAV = (Total Assets − Total Liabilities) ÷ Total Units Outstanding

Common NAV Misconception

Many investors mistakenly believe that a fund with a lower NAV (say ₹10) is “cheaper” and thus a better buy than a fund with a higher NAV (say ₹500). This is completely incorrect.

NAV by itself tells you nothing about value. A fund with NAV of ₹500 may have been growing steadily for 15 years and represent excellent value, while a new fund at ₹10 NAV may never recover from poor performance. What matters is the growth trajectory and underlying portfolio quality, not the absolute NAV figure.

Portfolio Turnover Ratio

What Is Portfolio Turnover?

The portfolio turnover ratio measures how frequently a fund buys and sells its holdings within a year. It is expressed as a percentage.

- High Turnover (above 100%): The fund manager frequently trades, incurring higher transaction costs and tax implications — which can reduce net returns.

- Low Turnover (below 30%): A buy-and-hold approach that reduces costs and is tax-efficient.

Index funds typically have turnover ratios of less than 10%, while some active funds churn their portfolios at 150–200% annually. High turnover without corresponding outperformance is a red flag.

AUM (Assets Under Management)

AUM refers to the total market value of all investments managed by a mutual fund at a given point in time.

Why AUM Matters

- Very small AUM (below ₹100 crore) can indicate a fund struggling to attract investors — which may affect liquidity.

- Very large AUM in small-cap or mid-cap funds can be a problem — it becomes harder to take meaningful positions in smaller companies without moving the market.

- For liquid and debt funds, larger AUM usually signals stability and better deal-making ability.

A fund’s AUM should always be evaluated in the context of its category, not in isolation.

Treynor Ratio

The Treynor Ratio (also called the reward-to-volatility ratio) is similar to the Sharpe Ratio but uses beta (systematic/market risk) instead of standard deviation (total risk) in the denominator.

Formula:

Treynor Ratio = (Fund Return − Risk-Free Rate) ÷ Beta

The Treynor Ratio is best used when comparing diversified funds that are part of a larger portfolio — since unsystematic (company-specific) risk has already been diversified away. A higher Treynor Ratio is better.

How to Compare Mutual Funds Using These Metrics

When evaluating and shortlisting mutual funds, follow this structured framework:

Step 1 — Define Your Goal Are you investing for wealth creation, regular income, tax saving, or capital preservation? This determines the right fund category.

Step 2 — Check Rolling Returns (3-Year, 5-Year, 10-Year) Don’t rely on point-to-point returns. Rolling returns show consistency across multiple market cycles.

Step 3 — Evaluate the Expense Ratio Always prefer the Direct Plan. Compare expense ratios within the same category. For passive funds, the expense ratio should be near 0.10%–0.20%.

Step 4 — Analyse the Sharpe Ratio Among similar funds with similar returns, pick the one with a higher Sharpe Ratio — it took less risk to deliver those returns.

Step 5 — Check Alpha Over Multiple Periods A fund with consistent positive alpha over 5+ years justifies active management costs.

Step 6 — Review Beta Based on Your Risk Appetite Aggressive investors can tolerate high-beta funds; conservative investors should look for beta below 0.8.

Step 7 — Assess Standard Deviation Especially important for goal-based investing. A fund with very high standard deviation is unsuitable for goals within 3 years.

Step 8 — Verify AUM and Fund House Track Record Check the fund house’s overall credibility, fund manager tenure, and whether AUM is appropriate for the fund’s strategy.

Common Mistakes Investors Make

1. Chasing Past Returns A fund that returned 45% last year is not guaranteed to repeat that performance. Evaluate consistency, not peak performance.

2. Ignoring the Expense Ratio Even a 0.5% difference in expense ratio can cost lakhs over a 20-year investment horizon.

3. Confusing Low NAV with Cheap Valuation NAV is just a price per unit, not a quality indicator.

4. Over-Diversification Holding 15–20 different mutual funds does not necessarily reduce risk — many funds in the same category hold overlapping stocks. Aim for 4–6 well-diversified funds.

5. Stopping SIPs During Market Crashes Market downturns are when SIPs work best — you accumulate more units at lower prices, averaging down your cost.

6. Ignoring Tax Implications Equity funds held under 1 year attract 20% Short-Term Capital Gains (STCG). Held over 1 year, gains above ₹1.25 lakh are taxed at 12.5% LTCG (post Budget 2024 rules in India).

FAQs About Mutual Fund Metrics

Q1. What is a good Sharpe Ratio for a mutual fund? Generally, a Sharpe Ratio above 1.0 is considered good. Above 2.0 is excellent. However, always compare Sharpe Ratios within the same fund category, not across different asset classes.

Q2. Is a higher expense ratio justified for actively managed funds? Only if the fund consistently delivers alpha above the additional cost. If a fund has a 1.5% expense ratio but only generates 0.5% alpha, the net benefit is negative.

Q3. Should I prefer low-beta or high-beta funds? It depends on your investment horizon and risk tolerance. For a 10+ year horizon, high-beta equity funds have historically rewarded patient investors well. For shorter horizons or if you are risk-averse, low-beta funds are more appropriate.

Q4. Does a fund’s NAV matter when choosing a mutual fund? No. NAV only tells you the current price per unit. What matters for comparison purposes is the fund’s returns, risk ratios, and portfolio quality — not its absolute NAV value.

Q5. What is the ideal expense ratio for an index fund? For index funds and ETFs, an expense ratio of 0.05% to 0.20% is considered very good. Anything above 0.50% for an index fund should prompt you to look for better alternatives.

Final Thoughts: Invest Smarter, Not Harder

Mutual funds are one of the most accessible, diversified, and professionally managed investment tools available to retail investors today. But simply putting money into a “top-rated” fund without understanding the underlying metrics is like buying a car based solely on its paint colour.

The metrics covered in this guide — expense ratio, Sharpe ratio, alpha, beta, standard deviation, Sortino ratio, NAV, portfolio turnover, AUM, and Treynor ratio — collectively paint a comprehensive picture of a fund’s cost, performance, and risk profile.

Here’s a quick recap of what to look for:

| Metric | What You Want |

|---|---|

| Expense Ratio | Lower is better |

| Sharpe Ratio | Higher is better (above 1 is good) |

| Alpha | Positive, consistent alpha |

| Beta | Matches your risk appetite |

| Standard Deviation | Lower for conservative goals |

| Sortino Ratio | Higher is better |

| Portfolio Turnover | Lower is generally better |

| AUM | Appropriate for fund’s strategy |

| Treynor Ratio | Higher is better for diversified funds |

Before making any investment, always read the Scheme Information Document (SID) and the Key Information Memorandum (KIM). Consider consulting a SEBI-registered financial advisor for personalised guidance.

Remember: The best mutual fund is not the one with the highest past return — it is the one best aligned with your financial goals, risk tolerance, investment horizon, and cost sensitivity.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial or investment advice. Please consult a qualified financial advisor before making investment decisions.