Table of Contents

India’s capital market is one of the fastest-growing in the world. With the Bombay Stock Exchange (BSE) and National Stock Exchange (NSE) serving as the twin pillars of financial activity, India now hosts a market capitalisation of over ₹330 trillion — a figure that has more than doubled in the last five years. For domestic and foreign institutional investors alike, the Indian capital market represents an unmatched combination of growth, liquidity, and diversification.

But raw market growth alone does not translate into returns. The difference between average investors and India’s biggest companies — from Reliance Industries and HDFC Group to Tata Sons, Bajaj Finance, and global FIIs (Foreign Institutional Investors) — lies in their disciplined adoption of proven investment strategies.

Did You Know? FIIs and DIIs (Domestic Institutional Investors) collectively manage over ₹80 trillion in Indian equities. Their strategic playbooks, while complex, are built on a handful of repeatable frameworks — all of which are accessible to informed retail investors too.

In this article, we break down the top 10 investment strategies that India’s biggest companies and institutional players use to generate consistently high returns in the Indian capital market. Whether you are a retail investor, a portfolio manager, or a corporate treasury officer, these insights will help you build a smarter, more resilient investment approach.

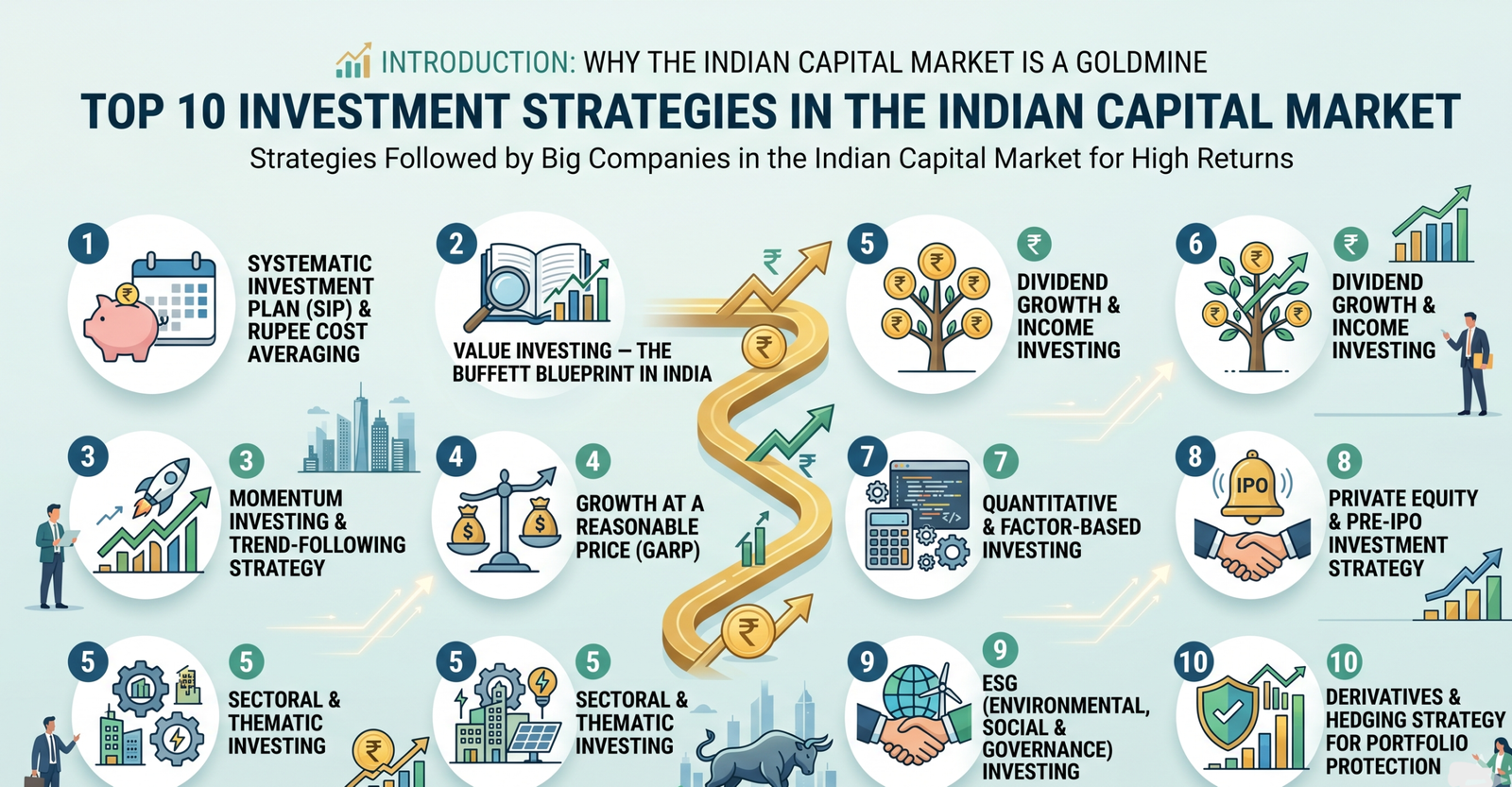

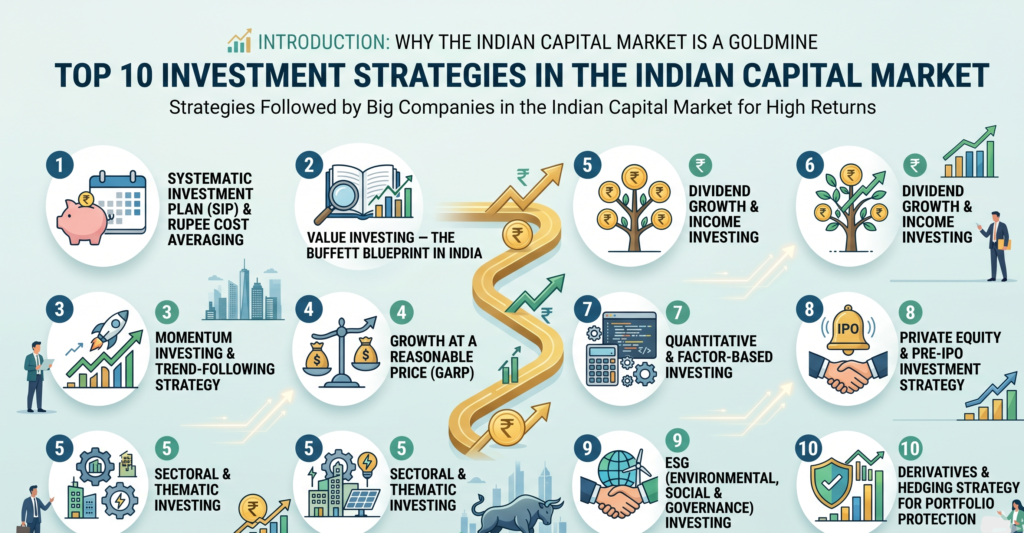

01

Low Risk · Compounding

Systematic Investment Plan (SIP) & Rupee Cost Averaging

The Systematic Investment Plan (SIP) is arguably the most widely practised institutional strategy in India today. While retail investors are familiar with monthly SIPs through mutual funds, large institutional players — including insurance giants like LIC, SBI Life, and corporate treasuries — use a structured version of this strategy called Rupee Cost Averaging (RCA) across equity portfolios, government securities, and corporate bond markets.

The mechanics are elegant: by investing a fixed corpus at regular intervals regardless of market conditions, companies accumulate more units when prices are low and fewer when prices are high. Over a full market cycle (typically 7–10 years), this strategy consistently outperforms lump-sum investments made at market peaks. India’s mutual fund industry crossed ₹53 trillion in AUM in 2024, with SIP inflows alone contributing over ₹19,000 crore every month — a testament to the strategy’s dominance.

Large conglomerates also extend this philosophy to treasury management: allocating surplus cash into liquid and debt mutual funds through systematic programmes rather than parking funds in low-yield savings accounts.

Key Takeaways

- Reduces the impact of short-term market volatility on overall portfolio cost

- Harnesses the power of compounding across equity and debt markets

- Reduces emotional decision-making — a discipline critical for large fund managers

- Best suited for long-term goals of 5 years and beyond

02

Fundamental · Long-Term

Value Investing — The Buffett Blueprint, Indian Edition

Value investing is the cornerstone strategy of some of India’s most celebrated investors and institutional funds. Inspired by Warren Buffett and Benjamin Graham’s principles, Indian players like Radhakishan Damani (founder of DMart), Rakesh Jhunjhunwala, and fund houses such as DSP Mutual Fund and Parag Parikh Financial Advisory Services (PPFAS) have built immense wealth by identifying fundamentally strong businesses trading below their intrinsic value.

The Indian capital market offers fertile ground for value investors. Due to the market’s occasional bouts of irrationality — driven by global FII outflows, geopolitical shocks, or domestic macroeconomic data — blue-chip and mid-cap companies often trade at significant discounts to their true worth. Skilled value investors use DCF (Discounted Cash Flow) analysis, Price-to-Book (P/B) ratios, and Price-to-Earnings (P/E) comparisons against historical averages and sectoral benchmarks to identify these opportunities.

“In the Indian context, value investing requires patience measured in years, not quarters. The biggest mistake is selling a great business too early.” — A leading Indian fund manager

Key Metrics Used

- P/E Ratio below industry average or historical mean

- Return on Equity (ROE) consistently above 15%

- Low Debt-to-Equity ratio (preferably below 0.5)

- Consistent free cash flow generation over 5+ years

- Promoter holding above 50% — a signal of conviction

03

Technical · Trend-Based

Momentum Investing & Trend-Following Strategy

Momentum investing operates on a simple but powerful premise: stocks that have performed well in the recent past tend to continue performing well in the near future. This strategy is extensively used by algorithmic trading desks of large brokerage firms, FIIs, and hedge funds operating in Indian markets through registered FPI (Foreign Portfolio Investor) routes.

In India, momentum is particularly strong in the mid-cap and small-cap segments of BSE and NSE. Studies of NSE data spanning two decades consistently show that a momentum portfolio — rebalanced quarterly by selecting the top 20% of stocks by 12-month returns — outperforms the Nifty 50 by 4–6% on an annualised basis. Institutional players using this strategy deploy sophisticated quantitative screens combined with moving average crossovers, Relative Strength Index (RSI) signals, and 52-week high breakouts to time their entries.

Companies like Kotak Mahindra AMC, Nippon India Mutual Fund, and major SEBI-registered Portfolio Management Services (PMS) firms run dedicated momentum-based funds that have delivered Nifty-beating returns over 3–5 year periods.

Tools & Indicators Used

- 12-month price momentum with 1-month reversal filter

- 200-day EMA (Exponential Moving Average) as trend filter

- RSI above 60 for entry confirmation

- High FII accumulation signals on NSE F&O data

04

Hybrid · Quality Growth

Growth at a Reasonable Price (GARP)

GARP — Growth at a Reasonable Price — is the hybrid strategy that bridges the gap between pure value investing and aggressive growth investing. Pioneered globally by Peter Lynch and widely adopted by India’s top institutional investors, GARP identifies companies with above-average earnings growth potential that are still available at valuations below their growth-adjusted fair value.

In practical terms, GARP investors in India look for companies where the PEG (Price/Earnings to Growth) ratio is below 1.5 — meaning the stock’s P/E multiple is comfortably supported by its earnings growth rate. Indian sectors like banking and financial services, pharmaceuticals, consumer discretionary, and information technology regularly produce GARP opportunities, especially during broader market corrections.

Large AMCs such as HDFC Mutual Fund and Axis Mutual Fund have historically run successful GARP-oriented large-cap schemes that have outperformed benchmarks over 10-year periods. For corporate treasuries managing long-term equity portfolios, GARP provides the discipline needed to avoid overpaying for growth while not missing genuinely transformative businesses.

GARP Screening Criteria

- EPS growth rate of 15–25% over 3 years

- PEG ratio below 1.5

- Sustainable competitive moat (brand, technology, regulation)

- Revenue growth aligned with earnings growth (no margin-compression growth)

05

Macro · Theme-Driven

Sectoral & Thematic Investing

Sectoral and thematic investing involves concentrating capital in specific sectors or macro themes expected to grow significantly over a 3–10 year horizon. This is one of the most actively used strategies by large Indian corporates, family offices, and domestic institutional investors (DIIs) who have the resources to conduct deep sectoral research.

India’s development journey has created several powerful multi-decade themes. The government’s PLI (Production Linked Incentive) schemes have triggered massive capital allocation into sectors like semiconductors, solar energy, defence manufacturing, and specialty chemicals. Big companies like Reliance Industries identified the telecom and digital infrastructure theme early, while the Tata Group made bold bets on electric vehicles and renewable energy well before they became consensus trades.

Current high-conviction thematic areas include digital infrastructure and data centres, green energy transition, defence indigenisation under Make in India, healthcare and diagnostics, and rural consumption growth. SEBI-approved thematic mutual fund schemes have proliferated, with AMCs launching dedicated Infrastructure, PSU, and Manufacturing funds that have posted exceptional 3-year returns.

High-Conviction Themes (2025)

- Green Energy: Solar, Wind, and Green Hydrogen

- Defence & Aerospace Manufacturing

- Digital Infrastructure: Data Centres, Cloud, AI

- Specialty Chemicals & Pharma APIs

- Rural Consumption & FMCG

06

Income · Steady Returns

Dividend Growth & Income Investing

Dividend growth investing focuses on companies that not only pay dividends but have a consistent track record of increasing their dividends year after year. This strategy is particularly favoured by insurance companies, pension funds, and large corporate treasuries that require predictable, recurring income streams alongside capital appreciation.

India’s PSU (Public Sector Undertaking) stocks — including ONGC, Coal India, Power Grid Corporation, and REC Limited — have historically been strong dividend payers, often yielding 4–8% annually in addition to potential capital gains. Private sector dividend champions include Infosys, TCS, ITC, and HCL Technologies. Large institutional holders of these stocks effectively earn a compounding income stream that, when reinvested, dramatically boosts long-term total returns.

Post the 2020 change in dividend taxation — where dividends are now taxed in the hands of investors at their applicable slab rate — corporates have become more strategic, prioritising companies with consistent buyback programmes alongside dividends to optimise post-tax returns.

Dividend Investing Criteria

- Dividend yield above 3% with a 5-year growth track record

- Payout ratio below 60% (ensures sustainability)

- Strong free cash flow coverage of dividends (1.5x or above)

- Low or zero debt on balance sheet

07

Data-Driven · Algo

Quantitative & Factor-Based Investing

Quantitative investing uses mathematical models, statistical analysis, and increasingly artificial intelligence to identify investment opportunities and manage risk. In India, this approach has gained enormous traction over the past decade, driven by the rise of algorithmic trading on NSE’s co-location servers and the proliferation of SEBI-registered quant PMS and AIF (Alternative Investment Fund) vehicles.

Factor-based investing — a systematic subset of quant investing — exploits specific risk-return drivers called “factors”. In the Indian context, the five most empirically validated factors are: Value (cheap stocks relative to fundamentals), Momentum (recent price strength), Quality (high ROE, low debt), Low Volatility (stable stocks), and Size (small and mid-caps). Combining multiple factors — often called a multi-factor strategy — has historically delivered significant alpha over the Nifty 500 in Indian backtests.

Institutional players such as DSP Quant Fund, Nippon India Quant Fund, and proprietary desks of leading brokerages run fully automated strategies that process thousands of data points — from earnings revision signals and options market data to satellite imagery of retail footfall — to generate investment signals at scale.

Key Factors Used in Indian Markets

- Quality Factor: ROE, ROCE, earnings stability

- Momentum Factor: 12-1 month price momentum

- Value Factor: EV/EBITDA, P/B relative to sector

- Low Volatility: Beta-adjusted portfolio construction

- Growth Factor: EPS revision momentum

08

High Risk · High Reward

Private Equity & Pre-IPO Investment Strategy

Private equity (PE) and pre-IPO investing represent the high-octane, high-conviction end of the investment spectrum. While restricted to sophisticated investors and institutions due to regulatory requirements under SEBI’s AIF framework, this strategy has generated some of the most spectacular returns in the Indian capital market over the past decade.

Indian conglomerates and family offices — including those managed by the Premji family (Wipro/Azim Premji Invest), Zerodha’s Nikhil Kamath, and major PE firms like ChrysCapital, Sequoia India (Peak XV Partners), and General Atlantic — have profited enormously by identifying India’s unicorn startups early. Companies like Zomato, Paytm, Nykaa, Delhivery, and Jio Financial Services created massive wealth for early institutional investors who entered at pre-IPO valuations.

The strategy involves identifying companies with strong unit economics, large addressable markets, scalable technology moats, and capable founders — then holding through the IPO window and beyond. With India’s IPO market consistently ranking among the world’s most active, this strategy continues to attract significant institutional capital.

Pre-IPO Investment Checklist

- TAM (Total Addressable Market) of ₹50,000 crore or above

- Path to profitability within 18–24 months of investment

- Strong founder pedigree and institutional co-investors

- Regulatory clearances and scalable unit economics

09

Future-Proof · Responsible

ESG (Environmental, Social & Governance) Investing

ESG investing has transitioned from a niche ethical preference to a mainstream institutional imperative in India. SEBI’s introduction of the Business Responsibility and Sustainability Report (BRSR) mandate for the top 1,000 listed companies, along with the global alignment of Indian capital markets with international ESG standards, has made ESG analysis a non-negotiable component of institutional due diligence.

Major global FIIs — including BlackRock, Vanguard, and Norges Bank Investment Management (Norway’s sovereign wealth fund) — have adopted strict ESG filters for their Indian equity allocations. Domestically, SBI Mutual Fund, ICICI Prudential AMC, and Quantum Mutual Fund have launched dedicated ESG funds that screen out companies with poor environmental records, weak governance structures, or unsustainable labour practices.

Beyond ethical considerations, the financial case for ESG investing in India is compelling. Studies show that BSE-listed companies with high ESG scores exhibit lower stock price volatility, better credit ratings, lower cost of capital, and superior long-term returns compared to ESG-laggards. As India accelerates its Net Zero 2070 commitment, ESG-aligned companies in renewables, sustainable manufacturing, and responsible finance are positioned for structural outperformance.

ESG Factors Evaluated

- E: Carbon footprint, water usage, waste management, renewable energy adoption

- S: Employee welfare, supply chain ethics, community impact, diversity

- G: Board independence, audit quality, promoter transparency, related-party transactions

- BRSR score and third-party ESG rating (MSCI, Sustainalytics)

10

Risk Management · Advanced

Derivatives & Hedging Strategy for Portfolio Protection

Derivatives-based hedging is the sophisticated risk management strategy used by virtually every large institutional investor in India to protect equity portfolios against market downturns while maintaining upside participation. India’s NSE F&O (Futures and Options) market is one of the largest in the world by contract volume — a reflection of the enormous institutional appetite for risk management tools.

Large companies and fund houses use several hedging techniques. Index put options on Nifty 50 and Bank Nifty act as insurance against broad market selloffs. Covered call writing on large-cap holdings generates additional income during sideways or mildly bullish markets. Futures-based delta hedging is used by portfolio managers to neutralise market-directional risk while retaining stock-specific alpha. Corporate treasuries also use currency futures and forwards on NSE/BSE to hedge foreign exchange exposure on import payables and export receivables.

The strategic use of derivatives is not speculation — it is insurance. Companies like Tata Consultancy Services, Infosys, and Wipro actively hedge their multi-billion dollar USD revenue exposure through structured forex derivatives programmes, directly protecting earnings and shareholder value from currency volatility.

Common Hedging Instruments in India

- Nifty Put Options — broad market downside protection

- Index Futures — short-term portfolio beta management

- Covered Call Writing — income generation on long equity holdings

- USD/INR Currency Futures — forex exposure hedging

- Interest Rate Swaps — corporate debt cost management

Conclusion: Building a Winning Investment Framework

The Indian capital market in 2025 is no longer a playing field only for specialists. With deepening market infrastructure, robust regulatory oversight by SEBI, and unprecedented access to financial data and analytical tools, the strategies used by India’s biggest companies are increasingly within reach of informed individual investors too.

The key insight from studying institutional behaviour is that no single strategy dominates in all market conditions. The most successful investors — whether they manage ₹500 crore or ₹5 lakh crore — combine multiple frameworks: value investing for the core portfolio, momentum for tactical allocations, ESG for risk filtration, and derivatives for downside protection.

What separates consistently successful investors is not superior intelligence — it is disciplined process, long-term conviction, and the ability to remain rational when markets are emotional. Study these strategies, adapt them to your risk profile and investment horizon, and approach the Indian capital market with the patience and rigour of a long-term institutional investor.

India’s greatest wealth-creation engine is its capital market. The question is not whether to participate — but how strategically you choose to do so.

Disclaimer: This article is published for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any securities. Investing in capital markets involves risk, including the possible loss of principal. Please consult a SEBI-registered investment advisor before making any investment decisions. Past performance is not indicative of future results.